A Registered Retirement Savings Plan (RRSP) is a savings plan registered with the Canadian federal government that you can contribute to for retirement purposes.

When you contribute money to an RRSP, your funds are “tax-advantaged,” meaning that they’re exempt from being taxed in the year you make the contribution. Any investment income earned from investments held within the RRSP can then grow tax-deferred as long as the money remains within the RRSP until it’s withdrawn.

RRSP contributions are tax-deductible, meaning they can be deducted from your current year’s tax return, potentially reducing the total amount of taxes you pay.

RRSP vs. RSP

RSPs (Retirement Savings Plans) and RRSPs are different names for the same retirement savings plan registered with the Federal Government.

What are the RRSP benefits you can bank on?

An RRSP is “Registered,” meaning that the CRA acknowledges the account – and your efforts at saving for your future. As a result, you’re rewarded with tax benefits, which you can take advantage of as soon as you open your RRSP account. Here are the two significant benefits:

- Pay less income tax: Each year, the amount of money you contribute to your RRSP (up to your allowable limit) can be deducted from your taxable income for that year – or a later year, if preferred, to pay less in taxes when your income may be higher. Simply put, you’ll receive either a bigger tax refund or a smaller tax bill each year you contribute. Eventually, you will pay tax when you withdraw the money from your RRSP account, but it will likely be at a lower tax rate because of your lower income in retirement.

- Enjoy tax-deferred investment growth: More than simply lowering the amount of income that you’ll be taxed on in the first place, you won’t pay taxes on your invested money – and the returns you earn inside an RRSP – until you withdraw it. In the meantime, any RRSP investment gains grow tax-free, helping you reach your savings goals more quickly.

The earlier you start contributing to an RRSP, the better, thanks to compound interest and upward market trends over time. If you invest money at age 26, for example, your sum has the potential to grow much larger than the same amount invested at age 36. And you don’t need a lot to get going.

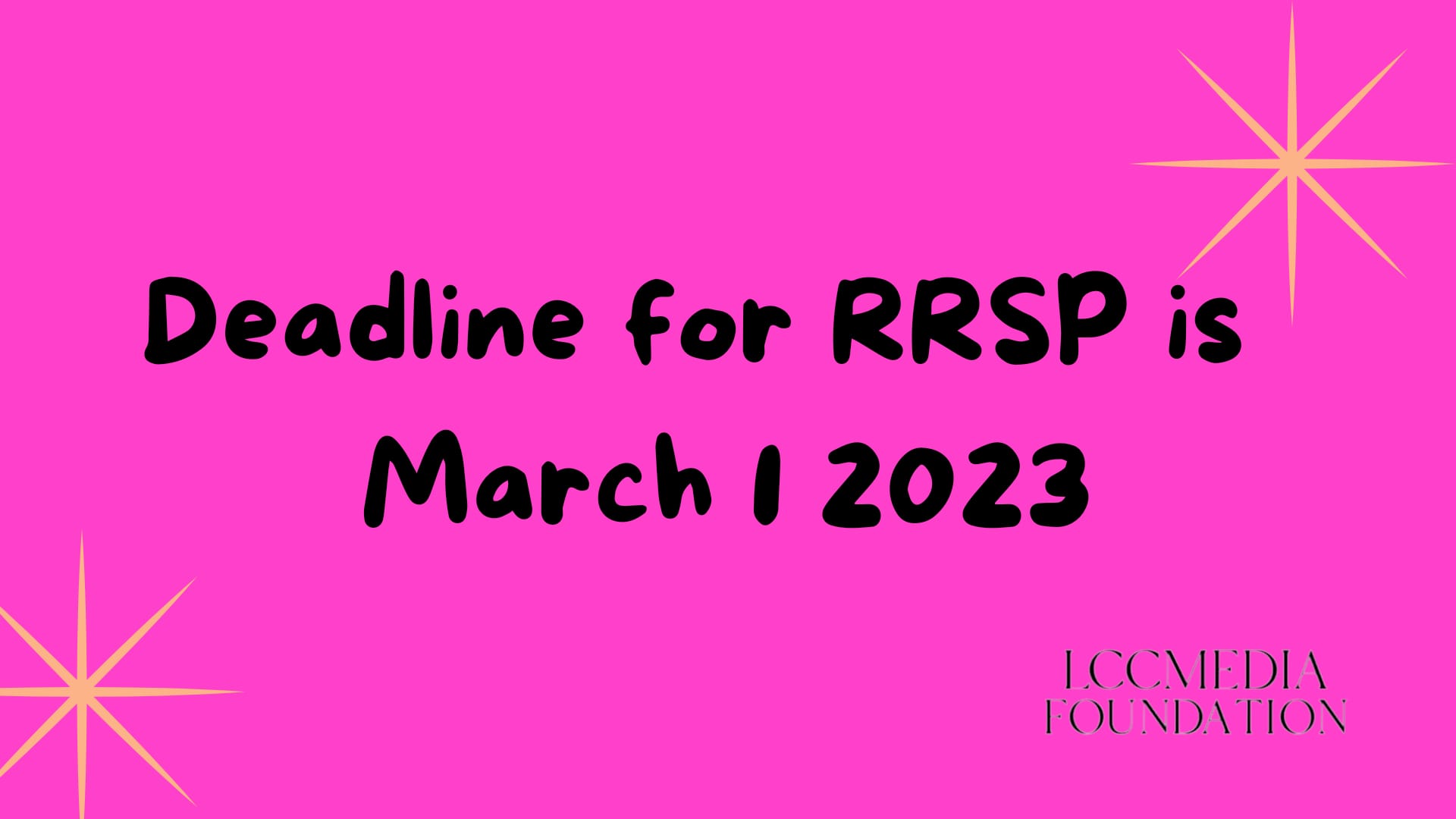

March 1, 2023, is the deadline to contribute to your RRSP for the 2022 tax year. This is the last day you can contribute to your RRSP if you want to take advantage of deductions and increase your tax return this spring.